The Intergovernmental Panel on Climate Change (IPCC) working group III (wg3) released its sixth assessment report (AR6) at the end of March, 2022. This post will summarize that IPCC AR6 wg3 report, which is likely to be the last major report from the IPCC before we all start melting like popsicles. See my previous posts for summaries of the working group 1 and working group 2 reports, published Aug 2021 and Feb 2022, respectively.

Current global GHG emissions and trends

I just read Bill Gate’s recent book, How to Avoid a Climate Disaster, and he puts annual greenhouse gas (GHG) emissions at 51 billion tonnes of CO2 equivalents (or gigatonnes, usually abbreviated in the IPCC reports as GtCO2-eq).

However, the latest IPPC report updates this figure to 59 billion tonnes of CO2 equivalents per year (59 GtCO2-eq / year), as of 2019.

Global net anthropogenic GHG emissions were 59±6.6 GtCO2-eq in 2019, about 12% higher than in 2010 and 54% higher than in 1990

Average annual GHG emissions during 2010-2019 were higher than in any previous decade, but the rate of growth between 2010 and 2019 was lower than that between 2000 and 2009.

So, global GHG emissions are higher than ever, the only glimmer of hope being that the rate of increase is slowing down. Obviously it needs to start decreasing, and fast, so this is a very small step in the right direction. Here’s a graph showing how much annual GHG emissions need to drop to achieve the goals to limit the increase in global temperature to 1.5°C or 2.0°C.

The two points on that graph, showing estimated GHG emissions for 2015 and 2019, suggest that we’d be lucky even to limit warming to 2.0°C (the purple line on the graph). Things need to change hard and fast to even have a chance of this, or even of limiting the increase at 3.0°C:

Without a strengthening of policies beyond those that are implemented by the end of 2020, GHG emissions are projected to rise beyond 2025, leading to a median global warming of 3.2°C by 2100.

Take a look at the reports from Working Group I and Working Group II to get an idea of how bad a 3.2°C in global temperature would be (spoiler alert – it’s not good!).

How do GHG emissions break down by sector?

In 2019, approximately 34% of total net anthropogenic GHG emissions came from the energy supply sector, 24% from industry, 22% from agriculture, forestry and other land use (AFOLU), 15% from transport and 6% from buildings.

However, adjustment should be made for the final users of the energy supply because 90% of emissions from electricity and heat production are due to the industry and buildings sectors.

So the breakdown looks more like this:

- Industry – 34%

- Agriculture, forestry and other land use (AFOLU) – 22%

- Buildings – 16%

- Transport – 15%

- Energy supply sector – 12%

Industry’s massive footprint is worth noting – one third of global GHG emissions – and that’s why corporate responsibility is crucial. The steel and concrete industries are major contributors (so construction projects can be large contributors to your personal carbon footprint) and the manufacturing of fertilizer and plastic also contribute significantly.

The amount of plastic manufactured in the US alone, generates an estimated 100 million tons of CO2 emissions. – California’s Plastic Problem.

Here’s a little more detail about where the rate of increase of GHG emissions is slowing down (or not):

Average annual GHG emissions growth between 2010 and 2019 slowed compared to the previous decade in energy supply [from 2.3% to 1.0%] and industry [from 3.4% to 1.4%], but remained roughly constant at about 2% per year in the transport sector (high confidence).

So actually transportation is not improving a lot, while energy supply (thanks to renewables and increase in efficiency) and industry are doing a bit better. Agriculture and land use change is harder to pinpoint but the main message was this:

About half of total net AFOLU emissions are from [land use change], predominantly from deforestation.

For this reason alone, it’s well worth paying attention when you buy meat, coffee, chocolate, and products that contain soy and palm oil. The solutions are sustainable agroforestry, shade grown coffee and cacao, avoiding meat as much as possible, knowing where your soy comes from, and avoiding the vast majority of palm oil (except Palm Done Right).

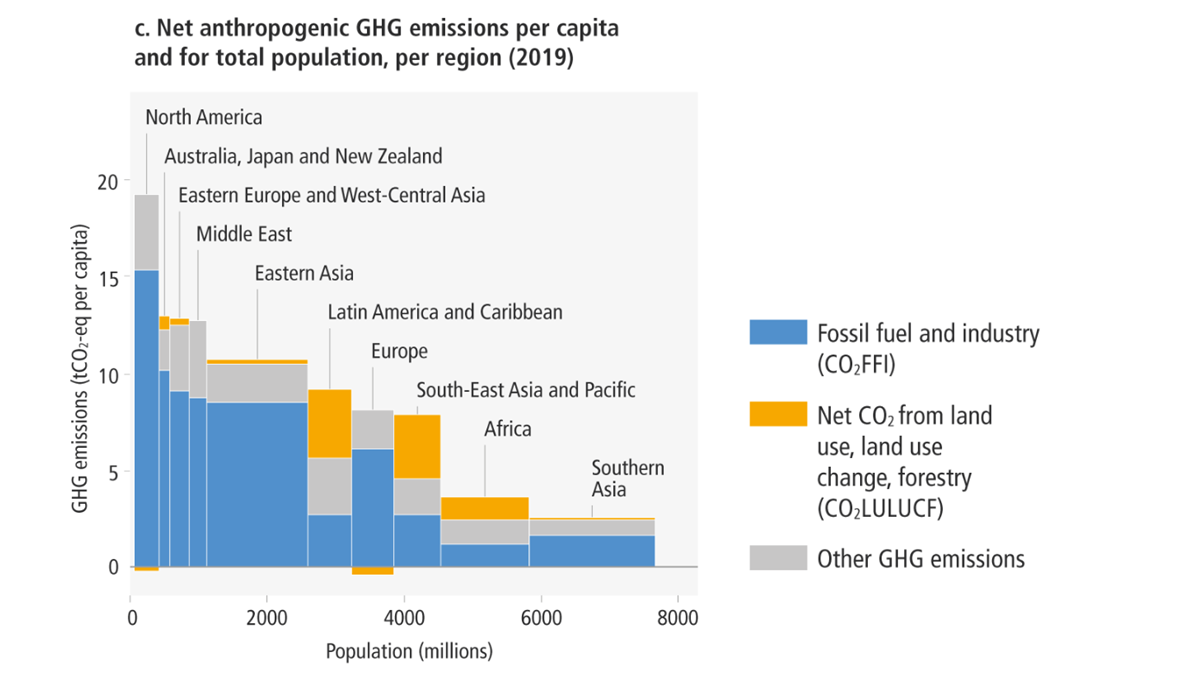

Greenhouse gas emissions per person

Average global per capita net anthropogenic GHG emissions increased from 7.7 to 7.8 tonnes CO2-equivalents (tCO2-eq), ranging from 2.6 tCO2-eq to 19 tCO2-eq across regions.

That was just helpful for me, thinking about my own carbon footprint (see this post on the CoolClimate calculator). If you live in the Global North, you’re probably doing pretty well if you’re around the global average. That’s because the average is brought down by the poorest folk in the world:

41% live in countries emitting less than 3 tCO2-eq per capita. A substantial share of the population in these low emitting countries lack access to modern energy services

I thought this was interesting and gave me hope:

Eradicating extreme poverty, energy poverty, and providing decent living standards to all in these regions in the context of achieving sustainable development objectives, in the near-term, can be achieved without significant global emissions growth.

Climate change – possible solutions from the IPCC

Like the other recent IPCC reports, there’s an emphasis on methane (CH4) reduction:

Due to the short lifetime of CH4 in the atmosphere, projected deep reduction of CH4 emissions up until the time of net zero CO2 in modelled mitigation pathways effectively reduces peak global warming. (high confidence)

The Working Group I report went into methane emissions in more detail – this underscores the number one thing that consumers can do to mitigate climate change: reduce meat intake. In the solutions suggested by Working Group III, there’s an emphasis on renewable energy, of course, and on achieving “a substantial reduction in overall fossil fuel use.” They also go into materials:

The use of steel, cement, plastics, and other materials is increasing globally, and in most regions. For almost all basic materials ‒ primary metals, building materials and chemicals ‒ many low- to zero- GHG intensity production processes are at the pilot to near-commercial and in some cases commercial stage but not yet established industrial practice.

Hydrogen direct reduction for primary steelmaking is near-commercial in some regions. Until new chemistries are mastered, deep reduction of cement process emissions will rely on already commercialized cementitious material substitution and the availability of Carbon Dioxide Capture and Storage (CCS).

Consumer demand & climate chance mitigation

Throughout the report the IPPC highlights the fact that climate mitigation isn’t just about government policy – consumer demand plays a very large role:

Demand-side measures and new ways of end-use service provision can reduce global GHG emissions in end use sectors by 40-70% by 2050.

Recommendations for climate-friendly consumer choices should come as no surprise:

low GHG intensive options such as sustainable healthy diets; food waste reduction; adaptive heating and cooling choices; integrated building renewable energy; and electric light-duty vehicles, and shifts to walking, cycling, shared pooled and public transit; sustainable consumption by intensive use of longer-lived repairable products (high confidence).

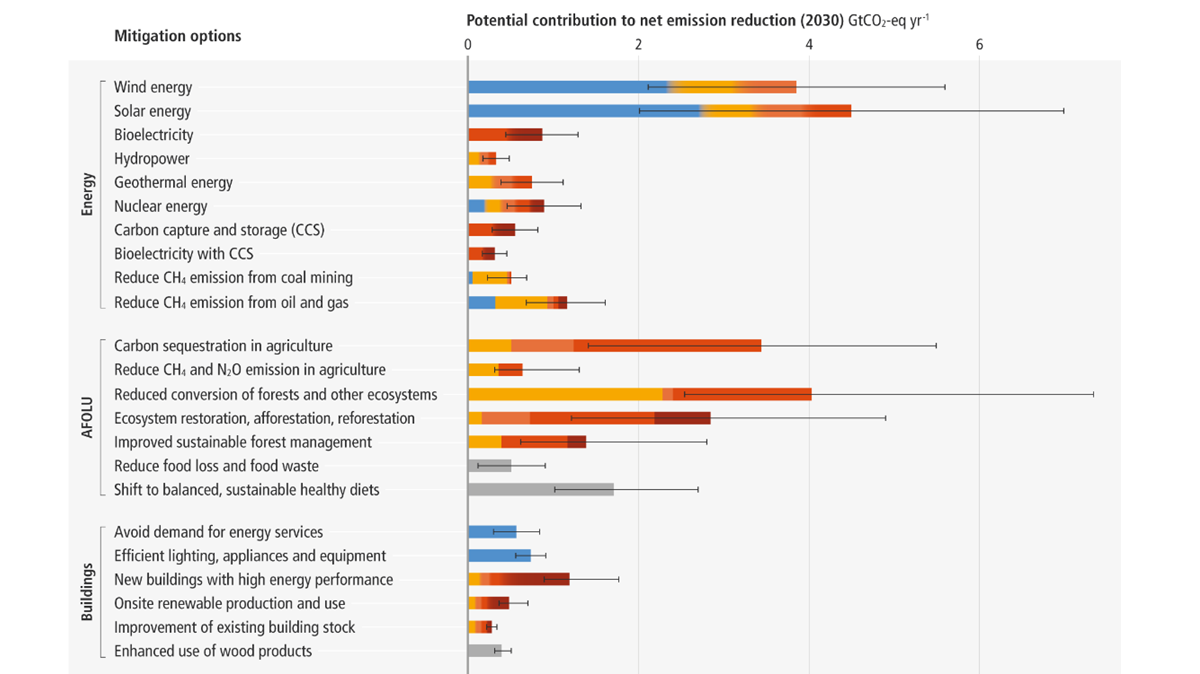

Low-cost, sustainable options for mitigating GHG emissions

One topic that captured attention in the media was the fact that large cuts in greenhouse gas emissions could be made at moderate cost. I wrote a post on this topic recently asking, can we offset global CO2 emissions? So, I was happy to see that the IPCC also pointed out the simple truth that we can make a lot of headway towards mitigating climate change with existing technology and programs, if we are willing to spend a little (relative to what we spent on Covid-19) money on it:

“Mitigation options costing USD100 tCO2-eq-1 or less could reduce global GHG emissions by at least half the 2019 level by 2030 (high confidence).

Options costing less than USD20 tCO2-eq-1 are estimated to make up more than half of this potential.

This number (USD20 tCO2-eq-1) means that it would cost less than $20 per tonne of CO2 mitigated/removed.

Large contributions with costs less than USD20 tCO2-eq-1 come from solar and wind energy, energy efficiency improvements, reduced conversion of natural ecosystems, and CH4 emissions reductions (coal mining, oil and gas, waste).

About 50–80% of CH4 emissions from these fossil fuels could be avoided with currently available technologies at less than USD50 tCO2-eq-1 (medium confidence).

The projected economic mitigation potential of AFOLU (Agriculture, forestry and other land use) options between 2020 and 2050, at costs below USD100 tCO2-eq-1, is 8-14 GtCO2-eq yr-1 (high confidence).

The largest share of this economic potential [4.2-7.4 GtCO2-eq yr-1] comes from the conservation, improved management, and restoration of forests and other ecosystems (coastal wetlands, peatlands, savannas and grasslands), with reduced deforestation in tropical regions having the highest total mitigation.

Improved and sustainable crop and livestock management, and carbon sequestration in agriculture, the latter includes soil carbon management in croplands and grasslands, agroforestry and biochar, can contribute 1.8-4.1 GtCO2-eq yr-1 reduction.

The global economic benefit of limiting warming to 2°C is reported to exceed the cost of mitigation in most of the assessed literature.

So it’s actually a net benefit, even on a purely economic level to use these measures to mitigate GHG emissions. It’s important to note that all of these things also contribute greatly to biodiversity, air quality, food security, and the biological integrity and resilience of our planet as a whole.

It’s good that the latest report is honing in on what needs to be said and matches with what many of us have felt and known for a long time.

Discover more from The Green Stars Project

Subscribe to get the latest posts sent to your email.

blood pressure medicine for you~https://soundcloud.com/kelly-bayer-1/plastic-tumbleweeds,

thank you for digesting eco knowledge for us jkaybay, been appreciating your blog!

LikeLike